ISSN 1004-5759 CN 62-1105/S

草业学报 ›› 2023, Vol. 32 ›› Issue (10): 226-246.DOI: 10.11686/cyxb2022471

• 综合评述 • 上一篇

秦涛1( ), 朱彩霞1(), 王建和2, 张瑾2

), 朱彩霞1(), 王建和2, 张瑾2

收稿日期:2022-11-30

修回日期:2023-01-12

出版日期:2023-10-20

发布日期:2023-07-26

通讯作者:

朱彩霞

作者简介:E-mail: 18137829506@163.com基金资助:

Tao QIN1(), Cai-xia ZHU1(), Jian-he WANG2, Jin ZHANG2

Received:2022-11-30

Revised:2023-01-12

Online:2023-10-20

Published:2023-07-26

Contact:

Cai-xia ZHU

摘要:

草原是我国重要的生态安全屏障、畜牧业基地以及碳库载体,构建以草原保险为核心的风险保障体系对于保护草原生态环境、促进牧区乡村振兴以及实现“双碳”目标具有重要价值。通过文献梳理以及定性比较分析,发现:美国、加拿大、法国等均建立了不同形式的草原保险产品体系,以指数保险为核心转移牧草风险,然而我国草原保险目前正处于探索和试点阶段,尚未建立比较符合我国国情的产品体系,在试点过程中,仍面临着保费筹集困难、推广模式缺乏统一性、产品供给动力不足、费率厘定缺乏理论依据以及定损理赔成本过高等诸多制约因素。因此,我国需要尽快完善草原保险政策制度与产品体系,构建央地保费补贴联动机制;健全多层次灾害风险保障体系,创新“综合保险+指数保险”发展模式;开发多样化草原保险产品,满足投保主体多元风险管理需求;推进草原风险区划与费率厘定,建立差异化动态定价机制;制定统一的查勘定损技术标准,优化完善核保理赔机制;提高草原保险科技水平,提升保险产品创新与服务能力。

秦涛, 朱彩霞, 王建和, 张瑾. 我国草原保险发展模式、现实困境与体系构建[J]. 草业学报, 2023, 32(10): 226-246.

Tao QIN, Cai-xia ZHU, Jian-he WANG, Jin ZHANG. Chinese grassland insurance development model, practical difficulties and system construction[J]. Acta Prataculturae Sinica, 2023, 32(10): 226-246.

保险类别 Class of insurance | 保险产品 Product of insurance | 实施国家与地区(时间) Implementation country and region (Time) |

|---|---|---|

天气指数保险 Weather index insurance | 牧草降水指数保险 Forage precipitation index insurance | 加拿大安大略省(2000年) Ontario,Canada (2000) |

| 美国得克萨斯州等6个州(2007年) Six states including Texas,USA (2007) | ||

| 德国(2014年) Germany (2014) | ||

| 奥地利(2015年) Austria (2015) | ||

| 瑞士(2016年)Switzerland (2016) | ||

植被指数保险 Vegetation index insurance | 牧草植被指数保险 Forage vegetation index insurance | 加拿大(2001年) Canada (2001) |

| 美国亚利桑那等8个州(2007年) 8 states including Arizona,USA (2007) | ||

| 法国(2015年) France (2015) |

表1 国外草原保险发展模式以及主要实施国家

Table 1 Foreign grassland insurance development models and main implementation countries

保险类别 Class of insurance | 保险产品 Product of insurance | 实施国家与地区(时间) Implementation country and region (Time) |

|---|---|---|

天气指数保险 Weather index insurance | 牧草降水指数保险 Forage precipitation index insurance | 加拿大安大略省(2000年) Ontario,Canada (2000) |

| 美国得克萨斯州等6个州(2007年) Six states including Texas,USA (2007) | ||

| 德国(2014年) Germany (2014) | ||

| 奥地利(2015年) Austria (2015) | ||

| 瑞士(2016年)Switzerland (2016) | ||

植被指数保险 Vegetation index insurance | 牧草植被指数保险 Forage vegetation index insurance | 加拿大(2001年) Canada (2001) |

| 美国亚利桑那等8个州(2007年) 8 states including Arizona,USA (2007) | ||

| 法国(2015年) France (2015) |

实施地区 Area of implementation | 加拿大(2000年) Canada (2000) | 美国(2007年) United States (2007) |

|---|---|---|

承保公司 Underwriting company | 农业保险公司Agricorp insurers | 美国农业风险自动管理部门—联邦作物保险公司与私人保险公司United States Department of Agriculture-Risk Management Authority and Federal Crop Insurance Corporation with private insurers |

投保主体 Subject of insurance | 牧场经营者、草料生产者。Rancher,forage producer. | 牧草经营者。Forage grass operator. |

保险标的 Subject matter of insurance | 牧场上正常生长的一年生或者多年生鲜牧草以及干草(其中干草只是改良后的牧场生产的)。Normal annual or perennial fresh forage and hay (where hay is produced only by improved pastures). | 可用于饲喂牲畜的一年生或者多年生鲜牧草或干草(投保牧草类别以及区域必须符合州市规定)。Annual or perennial fresh forage or hay that can be used to feed livestock (the type of forage and the area to be insured must meet state and municipal regulations). |

保险责任 Liability of insurance | 降水量不足与降水量过量(降水量过量只针对干草标的)。Insufficient and excessive precipitation (excessive precipitation only for hay barns). | 降水量不足。Lack of precipitation. |

保险金额 Amount of insurance | 保险金额取决于降水选项、牧场的改良程度(改良后的牧场价值每hm2在247.11~1581.47美元之间;未经改良的牧场价值每hm2在61.78~98.84美元之间)、选择的承保金额、与长期平均值相比的降水量和基于降水百分比的价格指数。The amount of insurance depends on the precipitation option,the degree of improvement of the pasture (the value of the improved ranch is between $247.11 and $1581.47 per hm2; The value of unimproved pastures is between $61.78 and $98.84 per hm2), the amount of coverage chosen,the amount of precipitation compared to the long-term average and a price index based on a percentage of precipitation. | 由标的物品种种类与县基准值共同决定。It is determined jointly by the subject matter variety and county reference value. |

保险期间 Period of insurance | 每年的5-8月共4个月期限(时间分辨率为单月、双月或3个月)。A total of 4 months from May to August each year (time resolution is one month,two months or three months). | 可以任意选择连续2个月的期限,最多可以选择 6 个不连续的区间(时间分辨率为2或7个月)。Choose any period of 2 consecutive months,up to 6 discontinuous intervals (time resolution 2 or 7 months). |

保险费率 Rate of insurance | 基于牧草作物价值、选择的覆盖值、覆盖选项(降水不足选项:客户基础保费率为2.64%,每个月加权之后为3.34%,3月加权后为4.42%;降水过多选项:5 mm阈值时为4.68%,7 mm阈值时为2.97%)、降水量收集站和收获期(仅限过量降水)区划厘定费率。Rates are determined based on forage crop values,selected cover values, cover options (precipitation deficit option: 2.64% for customers with a 1-month weighted premium rate of 3.34% after 1 month weighted and 4.42% after March weighting;Excessive rainfall options:4.68% at the 5 mm threshold,2.97% at the 7 mm threshold.),storm water collection stations and harvest times (excess precipitation only) zoning. | 鲜牧草费率相对较低,约为干草的1/3。Fresh forage rates are relatively low,about 1/3 of hay. |

财政补贴 Financial subsidy | 0 | 51%~59%( 保障水平90%时,政府补贴保费比例为51%;为80%和85%时,比例为55%;为70%和75%时,比例为59%)。51%-59% (when the protection level is 90%,the proportion of government subsidized premiums is 51%; 55% for 80% and 85%;59% for 70% and 75%). |

触发值 Trigger threshold | 降水不足选项:当单月降水量小于长期平均水平的85% 时则可触发赔偿;过量降水选项:若在收获期(第一次割草或干草时间)的10 d内,降水量≥5或7 mm,则可触发赔偿。Precipitation deficiency option:When the monthly precipitation is less than 85% of the long-term average,compensation can be triggered, excessive precipitation option:Compensation is triggered if the amount of precipitation is greater than 5 or 7 mm within 10 days of harvest (first mowing or hay time). | 当保险期内降水量低于平均降水量的70%~90%触发赔偿,至于具体触发值是70%~90%中的哪个值,则由农民自主选择。When the precipitation within the insurance period is lower than 70%-90% of the average precipitation,the compensation will be triggered. As for the specific trigger value of 70%- 90%, the farmers can choose independently. |

定损理赔 Settlement of loss and claim | 降水不足选项:超过85%的降水量无索赔,80%~85%按照一定比例计算降水指数。80%~85%的降水指数=(85%-降水百分比)×应用覆盖率×价格指数,80%的降水指数=[5%+(80%-降水百分比)×1.5)]×应用覆盖率×价格指数,额外增加5%表示从80%~85%的产量损失,低于长期平均值80%降水不足降水指数被计入1.5;过量降水选项:在预期的收获期内连续5 d的窗口降水量低于选择的阈值时将支付索赔,索赔=35%×选择的保险价值。Precipitation deficiency option:There is no claim for more than 85% of the precipitation,and 80%-85% of the precipitation index is calculated according to a certain proportion. If the precipitation is lower than the long-term average,80% of the precipitation deficiency is calculated as 1.5;Excess precipitation option: Claims will be paid when the window precipitation for five consecutive days during the expected harvest period falls below the selected threshold,claim=35%×selected insurance value. | 当降水指数低于由投保主体选择的保障水平决定的触发指数时,保险公司将支付赔款。赔款=(触发指数-降水指数)/触发指数×保障金额(降水指数=100+[(当前降水量-历史平均降水量)/历史平均降水量]×100,触发指数=100×保障指数。When the precipitation index is lower than the trigger index determined by the protection level selected by the insured entity,the insurance company will pay the compensation.Compensation=(trigger index-rainfall index)/trigger index×the amount of coverage (rainfall index=100+[(current rainfall-historical average rainfall)/historical average rainfall]×100,trigger index=100×protection index. |

表2 加拿大、美国两国牧草降水指数保险产品要素

Table 2 Elements of forage rainfall index insurance products in Canada and the United States

实施地区 Area of implementation | 加拿大(2000年) Canada (2000) | 美国(2007年) United States (2007) |

|---|---|---|

承保公司 Underwriting company | 农业保险公司Agricorp insurers | 美国农业风险自动管理部门—联邦作物保险公司与私人保险公司United States Department of Agriculture-Risk Management Authority and Federal Crop Insurance Corporation with private insurers |

投保主体 Subject of insurance | 牧场经营者、草料生产者。Rancher,forage producer. | 牧草经营者。Forage grass operator. |

保险标的 Subject matter of insurance | 牧场上正常生长的一年生或者多年生鲜牧草以及干草(其中干草只是改良后的牧场生产的)。Normal annual or perennial fresh forage and hay (where hay is produced only by improved pastures). | 可用于饲喂牲畜的一年生或者多年生鲜牧草或干草(投保牧草类别以及区域必须符合州市规定)。Annual or perennial fresh forage or hay that can be used to feed livestock (the type of forage and the area to be insured must meet state and municipal regulations). |

保险责任 Liability of insurance | 降水量不足与降水量过量(降水量过量只针对干草标的)。Insufficient and excessive precipitation (excessive precipitation only for hay barns). | 降水量不足。Lack of precipitation. |

保险金额 Amount of insurance | 保险金额取决于降水选项、牧场的改良程度(改良后的牧场价值每hm2在247.11~1581.47美元之间;未经改良的牧场价值每hm2在61.78~98.84美元之间)、选择的承保金额、与长期平均值相比的降水量和基于降水百分比的价格指数。The amount of insurance depends on the precipitation option,the degree of improvement of the pasture (the value of the improved ranch is between $247.11 and $1581.47 per hm2; The value of unimproved pastures is between $61.78 and $98.84 per hm2), the amount of coverage chosen,the amount of precipitation compared to the long-term average and a price index based on a percentage of precipitation. | 由标的物品种种类与县基准值共同决定。It is determined jointly by the subject matter variety and county reference value. |

保险期间 Period of insurance | 每年的5-8月共4个月期限(时间分辨率为单月、双月或3个月)。A total of 4 months from May to August each year (time resolution is one month,two months or three months). | 可以任意选择连续2个月的期限,最多可以选择 6 个不连续的区间(时间分辨率为2或7个月)。Choose any period of 2 consecutive months,up to 6 discontinuous intervals (time resolution 2 or 7 months). |

保险费率 Rate of insurance | 基于牧草作物价值、选择的覆盖值、覆盖选项(降水不足选项:客户基础保费率为2.64%,每个月加权之后为3.34%,3月加权后为4.42%;降水过多选项:5 mm阈值时为4.68%,7 mm阈值时为2.97%)、降水量收集站和收获期(仅限过量降水)区划厘定费率。Rates are determined based on forage crop values,selected cover values, cover options (precipitation deficit option: 2.64% for customers with a 1-month weighted premium rate of 3.34% after 1 month weighted and 4.42% after March weighting;Excessive rainfall options:4.68% at the 5 mm threshold,2.97% at the 7 mm threshold.),storm water collection stations and harvest times (excess precipitation only) zoning. | 鲜牧草费率相对较低,约为干草的1/3。Fresh forage rates are relatively low,about 1/3 of hay. |

财政补贴 Financial subsidy | 0 | 51%~59%( 保障水平90%时,政府补贴保费比例为51%;为80%和85%时,比例为55%;为70%和75%时,比例为59%)。51%-59% (when the protection level is 90%,the proportion of government subsidized premiums is 51%; 55% for 80% and 85%;59% for 70% and 75%). |

触发值 Trigger threshold | 降水不足选项:当单月降水量小于长期平均水平的85% 时则可触发赔偿;过量降水选项:若在收获期(第一次割草或干草时间)的10 d内,降水量≥5或7 mm,则可触发赔偿。Precipitation deficiency option:When the monthly precipitation is less than 85% of the long-term average,compensation can be triggered, excessive precipitation option:Compensation is triggered if the amount of precipitation is greater than 5 or 7 mm within 10 days of harvest (first mowing or hay time). | 当保险期内降水量低于平均降水量的70%~90%触发赔偿,至于具体触发值是70%~90%中的哪个值,则由农民自主选择。When the precipitation within the insurance period is lower than 70%-90% of the average precipitation,the compensation will be triggered. As for the specific trigger value of 70%- 90%, the farmers can choose independently. |

定损理赔 Settlement of loss and claim | 降水不足选项:超过85%的降水量无索赔,80%~85%按照一定比例计算降水指数。80%~85%的降水指数=(85%-降水百分比)×应用覆盖率×价格指数,80%的降水指数=[5%+(80%-降水百分比)×1.5)]×应用覆盖率×价格指数,额外增加5%表示从80%~85%的产量损失,低于长期平均值80%降水不足降水指数被计入1.5;过量降水选项:在预期的收获期内连续5 d的窗口降水量低于选择的阈值时将支付索赔,索赔=35%×选择的保险价值。Precipitation deficiency option:There is no claim for more than 85% of the precipitation,and 80%-85% of the precipitation index is calculated according to a certain proportion. If the precipitation is lower than the long-term average,80% of the precipitation deficiency is calculated as 1.5;Excess precipitation option: Claims will be paid when the window precipitation for five consecutive days during the expected harvest period falls below the selected threshold,claim=35%×selected insurance value. | 当降水指数低于由投保主体选择的保障水平决定的触发指数时,保险公司将支付赔款。赔款=(触发指数-降水指数)/触发指数×保障金额(降水指数=100+[(当前降水量-历史平均降水量)/历史平均降水量]×100,触发指数=100×保障指数。When the precipitation index is lower than the trigger index determined by the protection level selected by the insured entity,the insurance company will pay the compensation.Compensation=(trigger index-rainfall index)/trigger index×the amount of coverage (rainfall index=100+[(current rainfall-historical average rainfall)/historical average rainfall]×100,trigger index=100×protection index. |

图1 加拿大安大略省牧草降水指数保险运行模式

Fig. 1 Operation model of forage rainfall index insurance in Ontario,Canada

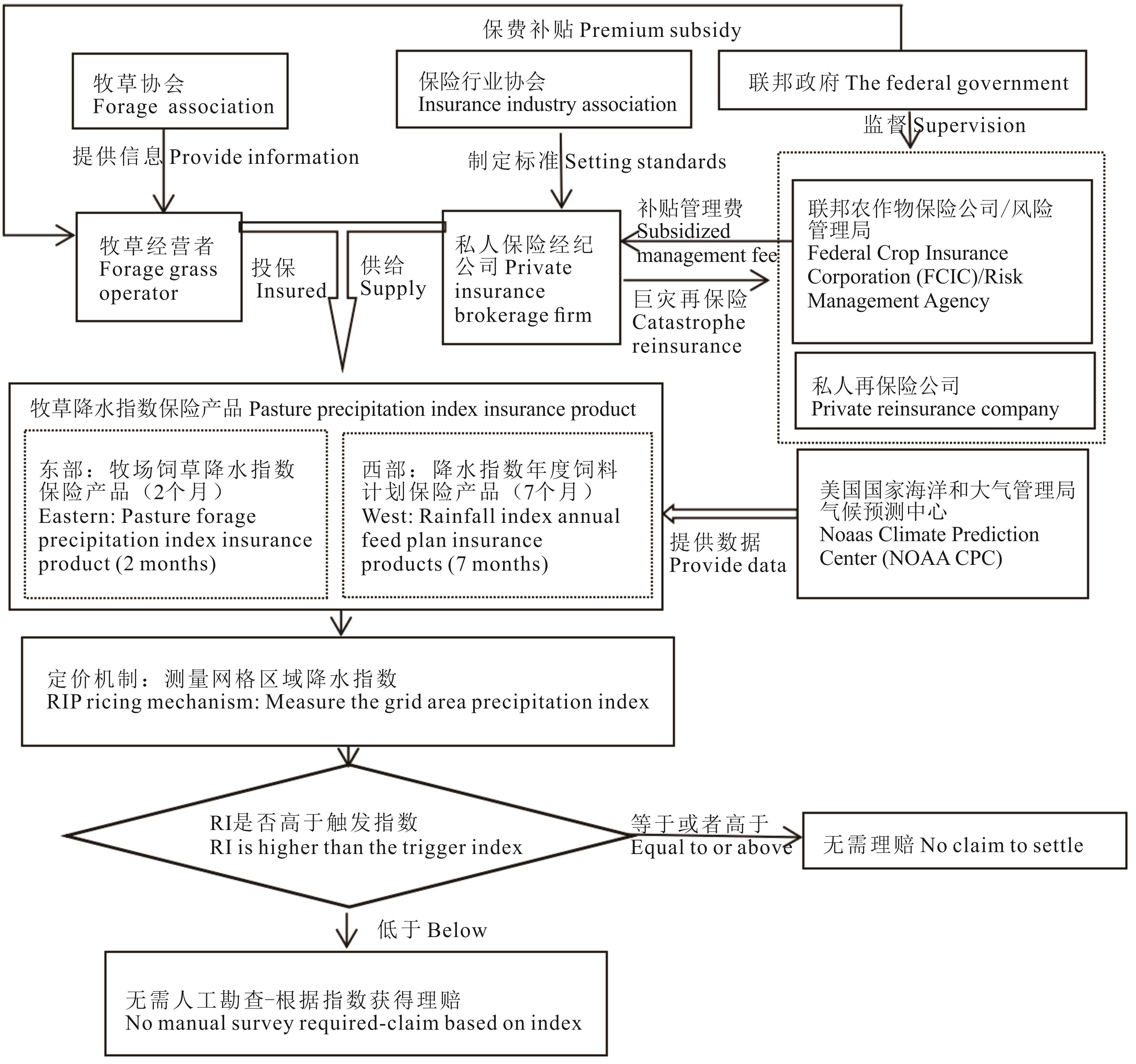

图2 美国牧草降水指数保险运行模式

Fig. 2 Operation model of forage precipitation index insurance in the United States

| 项目Item | 内容Content |

|---|---|

| 承保公司Underwriting company | 空中客车防务与航天公司Airbus Defense and Space |

| 投保主体Subject of insurance | 牧场牛、羊或混合饲养者。Ranch cattle,sheep,or mixed breeders. |

| 保险标的Subject matter of insurance | 草地正常生长的牧草。包括天然草地:种植多于6年;临时草地:种植少于6年;20%的禾本科,不包括人工草地。The normal growth of pasture. Including natural grasslands: Planted for more than 6 years; Temporary grassland: Planted for less than 6 years; 20% grasses,excluding artificial grass. |

| 保险责任Liability of insurance | 因为灾害造成的草地植被的减少从而导致的牧草产量的降低。The reduction of grassland vegetation caused by disasters leads to the reduction of forage yield. |

保险金额 Amount of insurance | 饲养员可根据草地类型调整选择保险金额和免赔额(10%~50%)。The breeder can adjust the insurance amount and deductible according to the grassland type (10% to 50%). |

| 保险期间Period of insurance | 1年。One year. |

| 保险费用Cost of insurance | 由饲养员对应于农场饲料回购的平均价格设定保险费用。保险保费在政府补贴前,缴费平均为 21 欧元·hm-2和 31 欧元·hm-2,即扣除补贴后分别为 10 欧元·hm-2和 14 欧元·hm-2。Insurance premiums are set by the breeder against the average price of farm feed repurchases. Insurance premiums are paid on average €21·hm-2 and €31·hm-2 before government subsidies, i.e. €10·hm-2and €14·hm-2 after deducting subsidies,respectively. |

| 保险费率Rate of insurance | 投保承保双方商定费率。The underwriting parties agree on the rate. |

| 财政补贴Financial subsidy | 补贴率平均50%,没有额外担保的合同可以达到 65%。Subsidy rates average around 50% and can reach 65% on contracts without additional guarantees. |

| 触发值Trigger threshold | 饲养员可以决定介于 20%~30% 之间的风险阈值,通常保险触发阈值平均为25%。The breeder can determine a risk threshold of between 20% and 30%,with the usual insurance trigger threshold averaging 25%. |

定损理赔 Settlement of loss and claim | 如果当年指数估计草地产量损失大于投保人的历史参考和选择的干预阈值,则无须事先声明,将自动向投保人支付赔偿,赔偿将按比例计算在每年5月1日— 9月30日期间因受保资本减去自付额而造成损失金额。If the index for the current year estimates grassland yield losses to be greater than the insured persons historical reference and selected intervention threshold,compensation will be automatically paid to the insured person, without prior statement,on a pro-rata basis for the amount of loss due to insured capital less co-payments for the period from 1 May to 30 September each year. |

表3 法国牧草植被指数保险产品要素

Table 3 Elements of forage vegetation index insurance products in France

| 项目Item | 内容Content |

|---|---|

| 承保公司Underwriting company | 空中客车防务与航天公司Airbus Defense and Space |

| 投保主体Subject of insurance | 牧场牛、羊或混合饲养者。Ranch cattle,sheep,or mixed breeders. |

| 保险标的Subject matter of insurance | 草地正常生长的牧草。包括天然草地:种植多于6年;临时草地:种植少于6年;20%的禾本科,不包括人工草地。The normal growth of pasture. Including natural grasslands: Planted for more than 6 years; Temporary grassland: Planted for less than 6 years; 20% grasses,excluding artificial grass. |

| 保险责任Liability of insurance | 因为灾害造成的草地植被的减少从而导致的牧草产量的降低。The reduction of grassland vegetation caused by disasters leads to the reduction of forage yield. |

保险金额 Amount of insurance | 饲养员可根据草地类型调整选择保险金额和免赔额(10%~50%)。The breeder can adjust the insurance amount and deductible according to the grassland type (10% to 50%). |

| 保险期间Period of insurance | 1年。One year. |

| 保险费用Cost of insurance | 由饲养员对应于农场饲料回购的平均价格设定保险费用。保险保费在政府补贴前,缴费平均为 21 欧元·hm-2和 31 欧元·hm-2,即扣除补贴后分别为 10 欧元·hm-2和 14 欧元·hm-2。Insurance premiums are set by the breeder against the average price of farm feed repurchases. Insurance premiums are paid on average €21·hm-2 and €31·hm-2 before government subsidies, i.e. €10·hm-2and €14·hm-2 after deducting subsidies,respectively. |

| 保险费率Rate of insurance | 投保承保双方商定费率。The underwriting parties agree on the rate. |

| 财政补贴Financial subsidy | 补贴率平均50%,没有额外担保的合同可以达到 65%。Subsidy rates average around 50% and can reach 65% on contracts without additional guarantees. |

| 触发值Trigger threshold | 饲养员可以决定介于 20%~30% 之间的风险阈值,通常保险触发阈值平均为25%。The breeder can determine a risk threshold of between 20% and 30%,with the usual insurance trigger threshold averaging 25%. |

定损理赔 Settlement of loss and claim | 如果当年指数估计草地产量损失大于投保人的历史参考和选择的干预阈值,则无须事先声明,将自动向投保人支付赔偿,赔偿将按比例计算在每年5月1日— 9月30日期间因受保资本减去自付额而造成损失金额。If the index for the current year estimates grassland yield losses to be greater than the insured persons historical reference and selected intervention threshold,compensation will be automatically paid to the insured person, without prior statement,on a pro-rata basis for the amount of loss due to insured capital less co-payments for the period from 1 May to 30 September each year. |

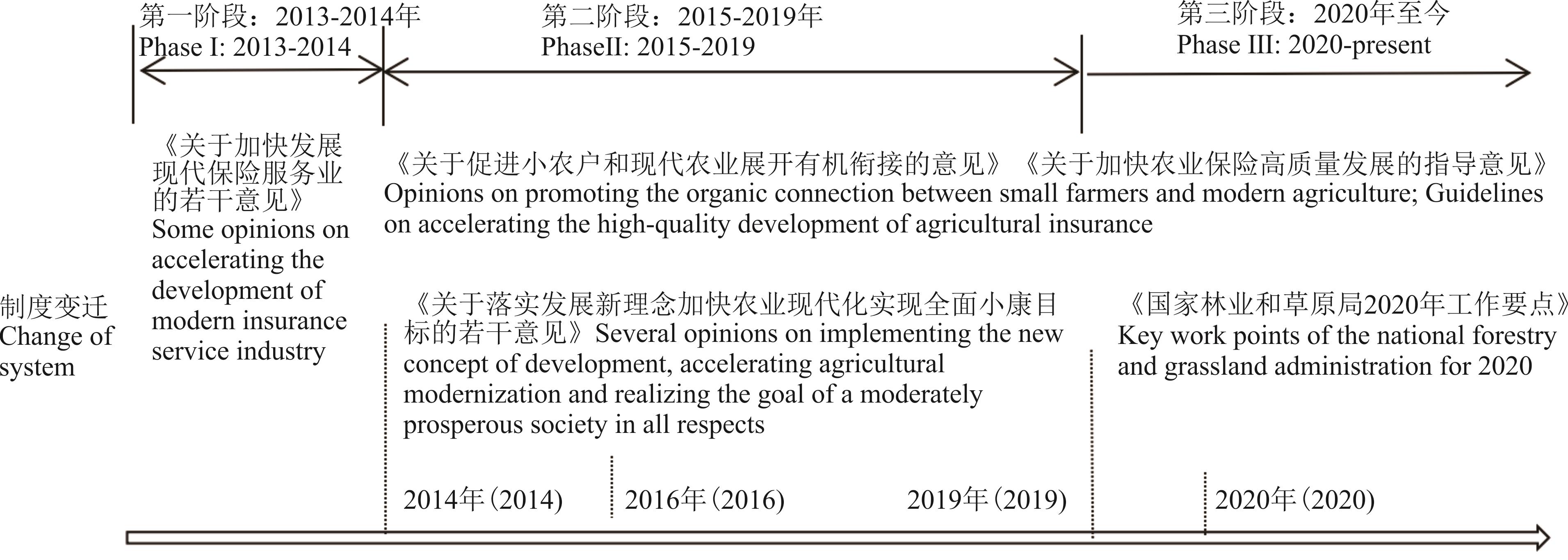

图3 我国草原保险制度变迁演进历程

Fig. 3 Evolution of Chinese grassland insurance system and evolution of pilot areas

保险类别 Class of insurance | 保险产品 Product of insurance | 试点地区与实施时间 Pilot area and implementation time |

|---|---|---|

综合保险 Comprehensive insurance | 草原综合保险 Grassland comprehensive insurance | 四川阿坝藏族羌族自治州红原县(2015年)。Hongyuan County,Aba Tibetan and Qiang Autonomous Prefecture,Sichuan Province (2015). |

| 内蒙古锡林浩特市白音库伦牧场(2016年)。Baiyinkulun Ranch,Xilinhot,Inner Mongolia (2016). | ||

| 内蒙古巴彦淖尔市乌拉特后旗(2020年)。Wulatehou Banner,Bayannur City,Inner Mongolia (2020). | ||

草场植被综合保险 Comprehensive grassland vegetation insurance | 内蒙古赤峰市阿鲁科尔沁旗(2016年)。Alukeerqin Banner,Chifeng City,Inner Mongolia (2016). | |

产量保险 Yield insurance | 牧草产量保险 Forage yield insurance | 西藏拉萨市达孜区(2019年)。Dazi District,Lhasa City,Tibet (2019). |

| 青海果洛州玛沁县(2021年)。Maqin County,Guoluo Prefecture,Qinghai Province (2021). | ||

指数保险 Index insurance | 牧草天气指数保险 Pasture weather index insurance | 内蒙古锡林郭勒盟苏尼特左旗(雪灾与旱灾)(2017年)。Sunite Left Banner,Xilingol League,Inner Mongolia (snow and drought) (2017). |

| 内蒙古呼伦贝尔市、兴安盟、通辽市、锡林郭勒盟(旱灾)(2020年)。Hulunbeier City,Xingan League,Tongliao City,Xilingol League of Inner Mongolia (drought) (2020). |

表4 我国草原保险发展模式与实施试点

Table 4 Chinese grassland insurance development mode and implementation of the pilot

保险类别 Class of insurance | 保险产品 Product of insurance | 试点地区与实施时间 Pilot area and implementation time |

|---|---|---|

综合保险 Comprehensive insurance | 草原综合保险 Grassland comprehensive insurance | 四川阿坝藏族羌族自治州红原县(2015年)。Hongyuan County,Aba Tibetan and Qiang Autonomous Prefecture,Sichuan Province (2015). |

| 内蒙古锡林浩特市白音库伦牧场(2016年)。Baiyinkulun Ranch,Xilinhot,Inner Mongolia (2016). | ||

| 内蒙古巴彦淖尔市乌拉特后旗(2020年)。Wulatehou Banner,Bayannur City,Inner Mongolia (2020). | ||

草场植被综合保险 Comprehensive grassland vegetation insurance | 内蒙古赤峰市阿鲁科尔沁旗(2016年)。Alukeerqin Banner,Chifeng City,Inner Mongolia (2016). | |

产量保险 Yield insurance | 牧草产量保险 Forage yield insurance | 西藏拉萨市达孜区(2019年)。Dazi District,Lhasa City,Tibet (2019). |

| 青海果洛州玛沁县(2021年)。Maqin County,Guoluo Prefecture,Qinghai Province (2021). | ||

指数保险 Index insurance | 牧草天气指数保险 Pasture weather index insurance | 内蒙古锡林郭勒盟苏尼特左旗(雪灾与旱灾)(2017年)。Sunite Left Banner,Xilingol League,Inner Mongolia (snow and drought) (2017). |

| 内蒙古呼伦贝尔市、兴安盟、通辽市、锡林郭勒盟(旱灾)(2020年)。Hulunbeier City,Xingan League,Tongliao City,Xilingol League of Inner Mongolia (drought) (2020). |

试点地区 Pilot areas | 四川阿坝州红原县(2015年) Hongyuan County,Aba Prefecture,Sichuan Province (2015) | 内蒙古锡林浩特市白音库伦牧场(2016年) Baiyinkulun Ranch,Xilinhot,Inner Mongolia (2016) | 内蒙古巴彦淖尔市乌拉特后旗(2020年) Wulatehou Banner,Bayannur City,Inner Mongolia (2020) |

|---|---|---|---|

投保主体 Subject of insurance | 管理和使用冬春草场的牧民(其中管理和使用冬春草场面积在33.33 hm2以上的牧民可单独投保,未达到33.33 hm2的,可以农业生产经营组织或村民委员会为单位组织牧民投保) A herdsman who manages and uses winter and spring pastures(Among them,herdsmen who manage and use winter and spring pastures with an area of more than 33.33 hm2 can be insured separately,and those who do not reach 33.33 hm2 can organize herdsmen to apply for insurance by agricultural production and operation organizations or villagers’committees) | 白音库伦牧场管理者 Baiyinkulun ranch manager | 拉嘎查村76户农牧民 76 farmers and herdsmen in Lagacha Village |

保险公司 Insurance company | 中航安盟财产保险有限公司 Groupama AVIC Insurance | 中华联合财产保险公司 China Insurance | 中国人民财产保险公司 Peoples Property Insurance Company of China |

保险标的 Subject matter of insurance | 用于生产干草的生长正常冬春草场 Normal winter and spring pasture used for hay production | 天然草场上生长正常的牧草 Normal grass grows on natural pastures | 禁牧区草原、草畜平衡区草原。Forbidden pastoral grassland,grass reserve equilibrium area. |

| 保险责任Liability of insurance | 旱灾、火灾、雹灾、洪灾 Droughts,fires,hail and floods | 火灾、虫灾和旱灾 Fires,insects and drought | 旱灾、病虫鼠害、沙尘暴和火灾 Droughts,pests,rats,sandstorms and fires |

保险金额 Amount of insurance | 1 yuan·hm-2 | 1.8 yuan·hm-2 | 1.33 yuan·hm-2。保险总金额也会根据牧草产量以及草原修复成本上下浮动协商调节。The total amount of insurance will also be adjusted according to the fluctuation of forage yield and grassland restoration costs. |

费率(保费) Rate (premium) | 8%(0.08 yuan·hm-2) | 5% (0.09 yuan·hm-2) | 5% (0.07 yuan·hm-2) |

财政补贴 Financial subsidy | 83%(县级财政补贴) 83% (fiscal subsidies from county-level ) | 80%(市级财政补贴) 80% (financial subsidy from municipal ) | 80%(自治区50%、盟市20%、旗县10%)。80% (50% from Autonomous Region,20% from League City, 10% from Banner County). |

保险期限 Term of insurance | 1年 1 year | 8个月(4-12月) 8 months (April-December) | 保险期限因保险责任而异(旱灾保险期间6个月: 4月1日至9月30日止,火灾、病虫鼠害、沙尘暴灾害保险期间为1个年度)。The period of insurance varies according to the insurance liability(Drought insurance period is 6 months: April 1 to September 30, fire, pest and rodent infestation, sandstorm disaster insurance period is 1 year). |

定损理赔 Settlement of loss and claim | 因火灾、雹灾直接造成损失且全损面积达到承保面积5%(含)以上,因旱灾、洪水直接造成损失且全损面积达到承保面积10%(含)以上,由保险公司负责赔偿。赔偿金额=每hm2保险金额×全损面积×(1-免赔率)。If the losses caused directly by fire and hail and the total loss area exceeds 5% (inclusive) of the insured area,the losses caused directly by drought and flood and the total loss area exceeds 10% (inclusive) of the insured area, the insurance company shall be responsible for the compensation. Compensation amount=total loss area×total loss area per hm2 insured amount×(1-deductible). | 理赔员通过现场拍照、标本取证对投保草场生长情况及受灾程度进行定损,依据损失面积进行理赔。Claims adjuster through on-site photos,specimen evidence on the growth of the insured grassland and the extent of the disaster loss, according to the loss area to settle claims. | 根据旗县级以上林草等部门发布的灾害报告(多部门联合以受灾草原不同灾害等级和对应损失面积确定赔偿标准)作为灾害事故发生的依据,根据保险责任启动保险赔偿。According to the disaster report issued by the forestry and grassland departments at or above the Bannel County level (multi-department joint determination of compensation standards based on different disaster levels and corresponding loss areas of the affected grassland) as the basis for the occurrence of a disaster accident, and the insurance compensation is initiated according to the insurance liability. |

表5 草原综合保险产品要素

Table 5 Grassland comprehensive insurance product elements

试点地区 Pilot areas | 四川阿坝州红原县(2015年) Hongyuan County,Aba Prefecture,Sichuan Province (2015) | 内蒙古锡林浩特市白音库伦牧场(2016年) Baiyinkulun Ranch,Xilinhot,Inner Mongolia (2016) | 内蒙古巴彦淖尔市乌拉特后旗(2020年) Wulatehou Banner,Bayannur City,Inner Mongolia (2020) |

|---|---|---|---|

投保主体 Subject of insurance | 管理和使用冬春草场的牧民(其中管理和使用冬春草场面积在33.33 hm2以上的牧民可单独投保,未达到33.33 hm2的,可以农业生产经营组织或村民委员会为单位组织牧民投保) A herdsman who manages and uses winter and spring pastures(Among them,herdsmen who manage and use winter and spring pastures with an area of more than 33.33 hm2 can be insured separately,and those who do not reach 33.33 hm2 can organize herdsmen to apply for insurance by agricultural production and operation organizations or villagers’committees) | 白音库伦牧场管理者 Baiyinkulun ranch manager | 拉嘎查村76户农牧民 76 farmers and herdsmen in Lagacha Village |

保险公司 Insurance company | 中航安盟财产保险有限公司 Groupama AVIC Insurance | 中华联合财产保险公司 China Insurance | 中国人民财产保险公司 Peoples Property Insurance Company of China |

保险标的 Subject matter of insurance | 用于生产干草的生长正常冬春草场 Normal winter and spring pasture used for hay production | 天然草场上生长正常的牧草 Normal grass grows on natural pastures | 禁牧区草原、草畜平衡区草原。Forbidden pastoral grassland,grass reserve equilibrium area. |

| 保险责任Liability of insurance | 旱灾、火灾、雹灾、洪灾 Droughts,fires,hail and floods | 火灾、虫灾和旱灾 Fires,insects and drought | 旱灾、病虫鼠害、沙尘暴和火灾 Droughts,pests,rats,sandstorms and fires |

保险金额 Amount of insurance | 1 yuan·hm-2 | 1.8 yuan·hm-2 | 1.33 yuan·hm-2。保险总金额也会根据牧草产量以及草原修复成本上下浮动协商调节。The total amount of insurance will also be adjusted according to the fluctuation of forage yield and grassland restoration costs. |

费率(保费) Rate (premium) | 8%(0.08 yuan·hm-2) | 5% (0.09 yuan·hm-2) | 5% (0.07 yuan·hm-2) |

财政补贴 Financial subsidy | 83%(县级财政补贴) 83% (fiscal subsidies from county-level ) | 80%(市级财政补贴) 80% (financial subsidy from municipal ) | 80%(自治区50%、盟市20%、旗县10%)。80% (50% from Autonomous Region,20% from League City, 10% from Banner County). |

保险期限 Term of insurance | 1年 1 year | 8个月(4-12月) 8 months (April-December) | 保险期限因保险责任而异(旱灾保险期间6个月: 4月1日至9月30日止,火灾、病虫鼠害、沙尘暴灾害保险期间为1个年度)。The period of insurance varies according to the insurance liability(Drought insurance period is 6 months: April 1 to September 30, fire, pest and rodent infestation, sandstorm disaster insurance period is 1 year). |

定损理赔 Settlement of loss and claim | 因火灾、雹灾直接造成损失且全损面积达到承保面积5%(含)以上,因旱灾、洪水直接造成损失且全损面积达到承保面积10%(含)以上,由保险公司负责赔偿。赔偿金额=每hm2保险金额×全损面积×(1-免赔率)。If the losses caused directly by fire and hail and the total loss area exceeds 5% (inclusive) of the insured area,the losses caused directly by drought and flood and the total loss area exceeds 10% (inclusive) of the insured area, the insurance company shall be responsible for the compensation. Compensation amount=total loss area×total loss area per hm2 insured amount×(1-deductible). | 理赔员通过现场拍照、标本取证对投保草场生长情况及受灾程度进行定损,依据损失面积进行理赔。Claims adjuster through on-site photos,specimen evidence on the growth of the insured grassland and the extent of the disaster loss, according to the loss area to settle claims. | 根据旗县级以上林草等部门发布的灾害报告(多部门联合以受灾草原不同灾害等级和对应损失面积确定赔偿标准)作为灾害事故发生的依据,根据保险责任启动保险赔偿。According to the disaster report issued by the forestry and grassland departments at or above the Bannel County level (multi-department joint determination of compensation standards based on different disaster levels and corresponding loss areas of the affected grassland) as the basis for the occurrence of a disaster accident, and the insurance compensation is initiated according to the insurance liability. |

试点地区 Pilot areas | 赤峰市阿鲁科尔沁旗(2016年) Alukeerqin Banner,Chifeng City (2016) |

|---|---|

| 投保主体Subject of insurance | 草场经营者Meadow operator |

| 保险公司Insurance company | 中航安盟财险有限公司内蒙古分公司 Groupama AVIC Insurance Inner Mongolia Branch |

| 保险标的Subject matter of insurance | 在天然草场上生长状况良好的牧草(无病虫害、种植管理正常)。Grass growing in good condition on natural pastures (no pests and diseases,normal planting management). |

| 保险责任Liability of insurance | 旱灾、火灾、鼠害、沙尘暴、暴雨、洪水、内涝、风灾、冻灾。Drought,fire,rat infestations,sandstorms,rainstorms,floods,water logging,wind and freezing. |

| 保险金额Amount of insurance | 2016年是900元·hm-2,2020年之后每hm2保险金额参照当地前5年平均产草量的70%与约定的成本单价,由投保人与保险人协商确定,并在保险单中注明。In 2016,it is 900 yuan·hm-2. After 2020,the insurance amount per hm2 shall refer to 70% of the average forage yield in the previous five years and the agreed unit price of cost,which shall be determined by the insurance applicant and insurer through consultation and indicated in the insurance policy. |

| 保险期间Period of insurance | 牧草生长全过程5-9月。The whole process of forage growth from May to September. |

| 保险费率Rate of insurance | 8%(72 yuan·hm-2) |

| 财政补贴Financial subsidy | 0 |

| 触发值Trigger threshold | 当“遥感数据+气象数据”数据持续异常,地面监测到灾害已发生且不可逆时,由牧草生长期内归一化植被指数计算因各种自然灾害导致的产草量损失确定灾害指数,不需要人工查勘确定根据灾害指数启动定损赔付(NDVI实际观测值以双方协商认同的第三方权威机构出具的数据为准)。When the data of “remote sensing data + meteorological data” continues to be abnormal and the disaster has occurred and is irreversible according to the ground monitoring,the forage yield loss caused by various natural disasters can be calculated by the normalized vegetation index during the growth period of herbage to determine the disaster index,and it is not necessary to conduct manual survey to determine the loss and compensation according to the disaster index(The actual observed value of NDVI shall be subject to the data issued by the third-party authority agreed upon by both parties). |

| 定损理赔Settlement of loss and claim | 保险人按照约定计算被保险人损失及赔偿金额。赔偿金额=保险金额×损失率,其中损失率=(约定单位面积产草量-实际单位面积产草量)/约定单位面积产草量,实际单位面积产草量=保险期内基于NDVI计算的单位面积产草量加权平均值;约定单位面积产草量=基于NDVI计算的当地前5年实际单位面积产草量的平均值×70%。The insurer shall calculate the insureds loss and compensation amount in accordance with the following provisions. Compensation amount=insured amount×loss rate, where loss rate=(agreed grass yield per unit area-actual grass yield per unit area)/agreed grass yield per unit area, actual grass yield per unit area=weighted average of grass yield per unit area calculated based on NDVI during the insurance period; Agreed grass yield per unit area=the average of the actual local grass production per unit area in the previous five years based on NDVI calculations×70%. |

表6 赤峰市牧草植被保险产品要素

Table 6 Forage vegetation insurance product elements in Chifeng City

试点地区 Pilot areas | 赤峰市阿鲁科尔沁旗(2016年) Alukeerqin Banner,Chifeng City (2016) |

|---|---|

| 投保主体Subject of insurance | 草场经营者Meadow operator |

| 保险公司Insurance company | 中航安盟财险有限公司内蒙古分公司 Groupama AVIC Insurance Inner Mongolia Branch |

| 保险标的Subject matter of insurance | 在天然草场上生长状况良好的牧草(无病虫害、种植管理正常)。Grass growing in good condition on natural pastures (no pests and diseases,normal planting management). |

| 保险责任Liability of insurance | 旱灾、火灾、鼠害、沙尘暴、暴雨、洪水、内涝、风灾、冻灾。Drought,fire,rat infestations,sandstorms,rainstorms,floods,water logging,wind and freezing. |

| 保险金额Amount of insurance | 2016年是900元·hm-2,2020年之后每hm2保险金额参照当地前5年平均产草量的70%与约定的成本单价,由投保人与保险人协商确定,并在保险单中注明。In 2016,it is 900 yuan·hm-2. After 2020,the insurance amount per hm2 shall refer to 70% of the average forage yield in the previous five years and the agreed unit price of cost,which shall be determined by the insurance applicant and insurer through consultation and indicated in the insurance policy. |

| 保险期间Period of insurance | 牧草生长全过程5-9月。The whole process of forage growth from May to September. |

| 保险费率Rate of insurance | 8%(72 yuan·hm-2) |

| 财政补贴Financial subsidy | 0 |

| 触发值Trigger threshold | 当“遥感数据+气象数据”数据持续异常,地面监测到灾害已发生且不可逆时,由牧草生长期内归一化植被指数计算因各种自然灾害导致的产草量损失确定灾害指数,不需要人工查勘确定根据灾害指数启动定损赔付(NDVI实际观测值以双方协商认同的第三方权威机构出具的数据为准)。When the data of “remote sensing data + meteorological data” continues to be abnormal and the disaster has occurred and is irreversible according to the ground monitoring,the forage yield loss caused by various natural disasters can be calculated by the normalized vegetation index during the growth period of herbage to determine the disaster index,and it is not necessary to conduct manual survey to determine the loss and compensation according to the disaster index(The actual observed value of NDVI shall be subject to the data issued by the third-party authority agreed upon by both parties). |

| 定损理赔Settlement of loss and claim | 保险人按照约定计算被保险人损失及赔偿金额。赔偿金额=保险金额×损失率,其中损失率=(约定单位面积产草量-实际单位面积产草量)/约定单位面积产草量,实际单位面积产草量=保险期内基于NDVI计算的单位面积产草量加权平均值;约定单位面积产草量=基于NDVI计算的当地前5年实际单位面积产草量的平均值×70%。The insurer shall calculate the insureds loss and compensation amount in accordance with the following provisions. Compensation amount=insured amount×loss rate, where loss rate=(agreed grass yield per unit area-actual grass yield per unit area)/agreed grass yield per unit area, actual grass yield per unit area=weighted average of grass yield per unit area calculated based on NDVI during the insurance period; Agreed grass yield per unit area=the average of the actual local grass production per unit area in the previous five years based on NDVI calculations×70%. |

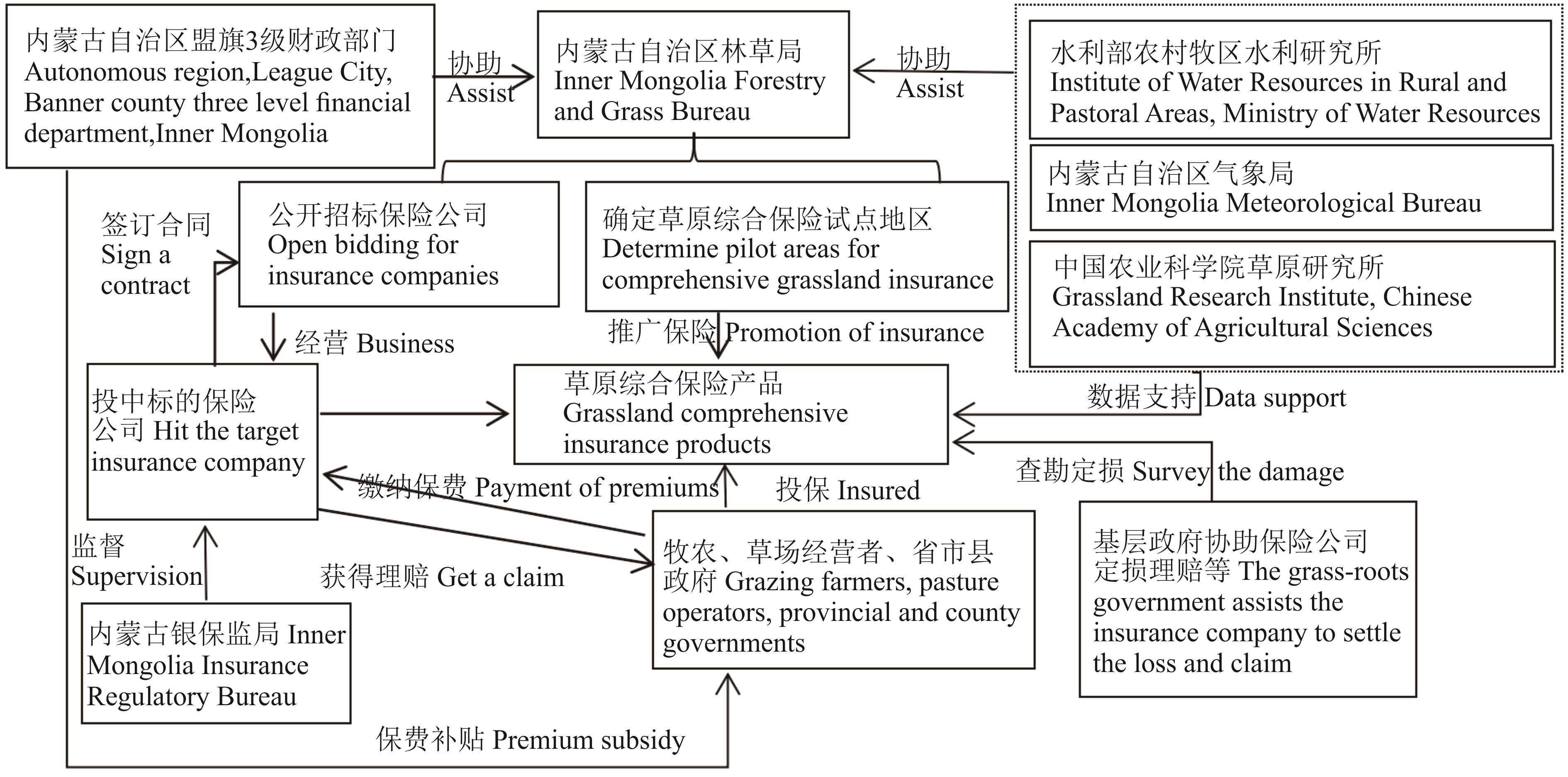

图4 内蒙古自治区草原综合保险运行模式

Fig. 4 Operation model of grassland comprehensive insurance in Inner Mongolia Autonomous Region

图5 赤峰市牧草植被保险运行模式

Fig. 5 Operation model of forage vegetation insurance in Chifeng City

试点地区 Pilot areas | 西藏拉萨市达孜区(2019年) Dazi District,Lhasa City,Tibet (2019) | 青海果洛州玛沁县(2021年) Maqin County,Guoluo Prefecture,Qinghai Province (2021) |

|---|---|---|

投保主体 Subject of insurance | 西藏农投牧业发展有限公司、新型经营主体、农牧民。Tibet Agricultural Investment and Animal Husbandry Development Co.,ltd.,new business subjects,farmers and herdsmen. | 青海省境内从事牧草种植的农牧户、合作社或企业。Farmers and herdsmen,cooperatives or enterprises engaged in herbage cultivation in Qinghai Province. |

保险公司 Insurance company | 中国人寿财产保险有限公司西藏分公司Tibet Branch of China Life & Property Limited Insurance Company | 中国人寿财产保险股份有限公司果洛州分公司Guoluo Branch of China Life & Property Limited Insurance Company |

保险标的 Subject matter of insurance | 牧草产量 Yield of forage grass | 牧草产量(符合当地种植规范和管理要求,经政府部门审定的合格品种,在当地种植一年以上生长正常的牧场)。Forage output (in line with local planting standards and management requirements,qualified varieties approved by government departments,local planting for more than one year of normal growth pasture). |

保险责任 Liability of insurance | 暴雨、洪水、旱灾、雪灾、病虫草鼠害等自然灾害。Rainstorms,floods,droughts,snowstorms,diseases, insects,rats and other natural disasters. | 牧草因自然灾害、意外事故、病虫鼠害等。Natural disasters,accidents, pests and rodents. |

保险金额 Amount of insurance | / | 根据牧草约定目标产量与约定价格确定(总保费金额30万元)。According to the agreed target yield and agreed price of forage (the total premium amount is 300000 yuan). |

保险期间 Period of insurance | 牧草生长全过程。Whole process of pasture growth. | 自保险牧草苗齐时起,至成熟收获时止。From the time of full seedling of the insured forage to the time of mature harvest. |

保险费率 Rate of insurance | / | 6% |

财政补贴 Financial subsidy | 90%(农业农村部金融支农创新试点项目补贴)。90% (Subsidy from the Pilot Project of Financial Support for Agriculture of the Ministry of Agriculture and Rural Affairs). | 0 |

保费自缴 Self-payment of premium | 10%(新型农业经营主体、企业或农户自缴)。10% (Paid by new agricultural operators, enterprises or farmers). | 100%(总保险费1.8万元)。100%(Total insurance premium is 18000 yuan). |

定损理赔 Settlement of loss and claim | 以试点区域在一定时期内当雨水稀少、灌溉不足、意外等原因导致的平均产量低于阈值为理赔基础,损失补偿为实际平均产量与基础平均产量的差额。In a certain period of time,when the average yield of the pilot area is lower than the threshold due to reasons such as scarce rain,insufficient irrigation and accidents,the compensation for loss is the difference between the actual average yield and the basic average yield. | 当投保人保险期间实际产量低于每hm2约定预期产量则触发理赔机制。When the actual yield of the insurance applicant is lower than the agreed expected yield per hm2,the claim settlement mechanism will be triggered. |

表7 牧草产量保险产品要素

Table 7 Elements of forage yield insurance products

试点地区 Pilot areas | 西藏拉萨市达孜区(2019年) Dazi District,Lhasa City,Tibet (2019) | 青海果洛州玛沁县(2021年) Maqin County,Guoluo Prefecture,Qinghai Province (2021) |

|---|---|---|

投保主体 Subject of insurance | 西藏农投牧业发展有限公司、新型经营主体、农牧民。Tibet Agricultural Investment and Animal Husbandry Development Co.,ltd.,new business subjects,farmers and herdsmen. | 青海省境内从事牧草种植的农牧户、合作社或企业。Farmers and herdsmen,cooperatives or enterprises engaged in herbage cultivation in Qinghai Province. |

保险公司 Insurance company | 中国人寿财产保险有限公司西藏分公司Tibet Branch of China Life & Property Limited Insurance Company | 中国人寿财产保险股份有限公司果洛州分公司Guoluo Branch of China Life & Property Limited Insurance Company |

保险标的 Subject matter of insurance | 牧草产量 Yield of forage grass | 牧草产量(符合当地种植规范和管理要求,经政府部门审定的合格品种,在当地种植一年以上生长正常的牧场)。Forage output (in line with local planting standards and management requirements,qualified varieties approved by government departments,local planting for more than one year of normal growth pasture). |

保险责任 Liability of insurance | 暴雨、洪水、旱灾、雪灾、病虫草鼠害等自然灾害。Rainstorms,floods,droughts,snowstorms,diseases, insects,rats and other natural disasters. | 牧草因自然灾害、意外事故、病虫鼠害等。Natural disasters,accidents, pests and rodents. |

保险金额 Amount of insurance | / | 根据牧草约定目标产量与约定价格确定(总保费金额30万元)。According to the agreed target yield and agreed price of forage (the total premium amount is 300000 yuan). |

保险期间 Period of insurance | 牧草生长全过程。Whole process of pasture growth. | 自保险牧草苗齐时起,至成熟收获时止。From the time of full seedling of the insured forage to the time of mature harvest. |

保险费率 Rate of insurance | / | 6% |

财政补贴 Financial subsidy | 90%(农业农村部金融支农创新试点项目补贴)。90% (Subsidy from the Pilot Project of Financial Support for Agriculture of the Ministry of Agriculture and Rural Affairs). | 0 |

保费自缴 Self-payment of premium | 10%(新型农业经营主体、企业或农户自缴)。10% (Paid by new agricultural operators, enterprises or farmers). | 100%(总保险费1.8万元)。100%(Total insurance premium is 18000 yuan). |

定损理赔 Settlement of loss and claim | 以试点区域在一定时期内当雨水稀少、灌溉不足、意外等原因导致的平均产量低于阈值为理赔基础,损失补偿为实际平均产量与基础平均产量的差额。In a certain period of time,when the average yield of the pilot area is lower than the threshold due to reasons such as scarce rain,insufficient irrigation and accidents,the compensation for loss is the difference between the actual average yield and the basic average yield. | 当投保人保险期间实际产量低于每hm2约定预期产量则触发理赔机制。When the actual yield of the insurance applicant is lower than the agreed expected yield per hm2,the claim settlement mechanism will be triggered. |

图6 西藏牧草产量保险运行模式

Fig. 6 Operation model of forage yield insurance in Tibet

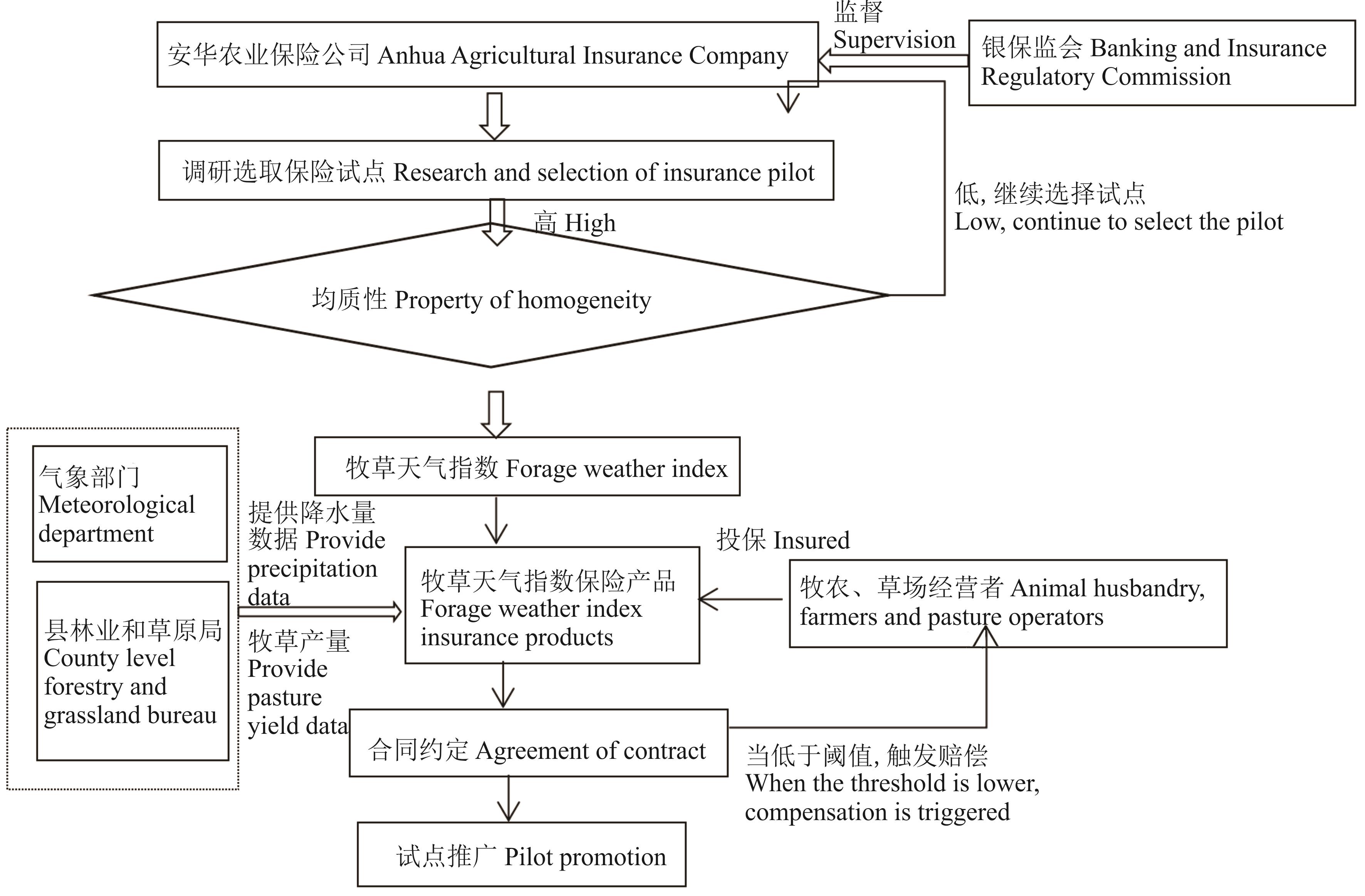

图7 兴安盟牧草天气指数保险运行模式

Fig. 7 Operation model of forage weather index insurance in Xing’an League

试点地区 Pilot areas | 内蒙古兴安盟(2020年) Xing’ an League, Inner Mongolia (2020) |

|---|---|

承保公司 Underwriting company | 安华农业保险公司内蒙古分公司 Inner Mongolia Branch of Anhua Agricultural Insurance Company |

投保主体 Subject of insurance | 牧民、牧区生产经营者。 Producers and operators in herdsmen and pastoral areas. |

保险标的 Subject matter of insurance | 集中连片种植于纯牧区草原的牧草。Concentrated and contiguous grasslands planted in pure pastoral areas. |

保险责任 Liability of insurance | 降水量不足。Lack of precipitation. |

保险金额 Amount of insurance | 保险金额=每hm2产量(kg·hm-2)×每hm2单价(yuan·kg-1)×保险面积(hm2)。每hm2产量是指牧草的干草量,具体每hm2产量和每hm2单价由投保人和保险人协商确定。Insurance amount=Yield per hm2 (kg·hm-2)×unit price per hm2 (Yuan·kg-1)×insured area (hm2). The yield per hm2 refers to the hay quantity of forage,and the specific yield per hm2 and the unit price per hm2 shall be determined by the insurance applicant and the insurer through negotiation. |

保险期间 Period of insurance | 牧草生长全过程,包括返青-展叶期(当年4月21日-5月20日)、拔节-分枝期(当年5月21日-6月20日)和现蕾-开花期(当年6月21日-7月31日)。The whole process of pasture growth,including regreening-leaf-spreading stage (21 April to 20 May that year), joint-branching stage (21 May to 20 June that year) and budding-flowering stage (21 June to 31 July that year). |

触发值 Trigger threshold | 当降水量小于阈值,保险公司将支付赔款,单个生长周期降水量低于保险合同的“牧草生长期降水量赔偿区间及比例表”中相应生长期降水量时,则视为保险事故发生,保险人按照保险合同的约定进行赔偿。When the precipitation is less than the threshold value, the insurance company will pay compensation, and when the precipitation in a single growth cycle is lower than the corresponding precipitation in the growth period in the “Compensation interval and scale Table of precipitation in the growth period of forage grass ” in the insurance contract, it will be regarded as an insurance accident, and the insurer will make compensation according to the agreement of the insurance contract. |

定损理赔 Settlement of loss and claim | 保险事故发生时,保险人按照投保地区的“牧草生长期降水量赔偿区间及比例表”中的赔偿比例进行赔偿。具体赔偿公式为:单个生长周期赔偿金额=保险金额×对应的赔偿比例;总赔偿金额=∑各生长周期赔偿金额。保险人按发生保险事故的次数分次进行赔偿,累计最高赔偿金额以保险金额为限。When an insured accident occurs,the insurer shall compensate according to the compensation ratio in the “Compensation range and proportion Table of precipitation in the forage growth period”in the insured area. The specific compensation formula is:Single growth cycle compensation amount=insurance amount×corresponding compensation ratio;Total compensation amount=∑compensation amount for each growth cycle. The insurer shall compensate according to the number of insured events,and the maximum cumulative compensation amount shall be limited to the insured amount. |

表8 兴安盟牧草干旱天气指数保险产品要素

Table 8 Elements of insurance products for drought weather index of forage in Xing’an League

试点地区 Pilot areas | 内蒙古兴安盟(2020年) Xing’ an League, Inner Mongolia (2020) |

|---|---|

承保公司 Underwriting company | 安华农业保险公司内蒙古分公司 Inner Mongolia Branch of Anhua Agricultural Insurance Company |

投保主体 Subject of insurance | 牧民、牧区生产经营者。 Producers and operators in herdsmen and pastoral areas. |

保险标的 Subject matter of insurance | 集中连片种植于纯牧区草原的牧草。Concentrated and contiguous grasslands planted in pure pastoral areas. |

保险责任 Liability of insurance | 降水量不足。Lack of precipitation. |

保险金额 Amount of insurance | 保险金额=每hm2产量(kg·hm-2)×每hm2单价(yuan·kg-1)×保险面积(hm2)。每hm2产量是指牧草的干草量,具体每hm2产量和每hm2单价由投保人和保险人协商确定。Insurance amount=Yield per hm2 (kg·hm-2)×unit price per hm2 (Yuan·kg-1)×insured area (hm2). The yield per hm2 refers to the hay quantity of forage,and the specific yield per hm2 and the unit price per hm2 shall be determined by the insurance applicant and the insurer through negotiation. |

保险期间 Period of insurance | 牧草生长全过程,包括返青-展叶期(当年4月21日-5月20日)、拔节-分枝期(当年5月21日-6月20日)和现蕾-开花期(当年6月21日-7月31日)。The whole process of pasture growth,including regreening-leaf-spreading stage (21 April to 20 May that year), joint-branching stage (21 May to 20 June that year) and budding-flowering stage (21 June to 31 July that year). |

触发值 Trigger threshold | 当降水量小于阈值,保险公司将支付赔款,单个生长周期降水量低于保险合同的“牧草生长期降水量赔偿区间及比例表”中相应生长期降水量时,则视为保险事故发生,保险人按照保险合同的约定进行赔偿。When the precipitation is less than the threshold value, the insurance company will pay compensation, and when the precipitation in a single growth cycle is lower than the corresponding precipitation in the growth period in the “Compensation interval and scale Table of precipitation in the growth period of forage grass ” in the insurance contract, it will be regarded as an insurance accident, and the insurer will make compensation according to the agreement of the insurance contract. |

定损理赔 Settlement of loss and claim | 保险事故发生时,保险人按照投保地区的“牧草生长期降水量赔偿区间及比例表”中的赔偿比例进行赔偿。具体赔偿公式为:单个生长周期赔偿金额=保险金额×对应的赔偿比例;总赔偿金额=∑各生长周期赔偿金额。保险人按发生保险事故的次数分次进行赔偿,累计最高赔偿金额以保险金额为限。When an insured accident occurs,the insurer shall compensate according to the compensation ratio in the “Compensation range and proportion Table of precipitation in the forage growth period”in the insured area. The specific compensation formula is:Single growth cycle compensation amount=insurance amount×corresponding compensation ratio;Total compensation amount=∑compensation amount for each growth cycle. The insurer shall compensate according to the number of insured events,and the maximum cumulative compensation amount shall be limited to the insured amount. |

| 1 | Allan R P, Soden B J. Atmospheric warming and the amplification of precipitation extremes. Science, 2008, 321(5895): 1481-1484. |

| 2 | Cui C, Wang M L, Hu X D. Grass and animal husbandry in China: Status quo, issues and policy suggestions-based on investigation in pilot areas of grass and animal husbandry in Shanxi and Qinghai Provinces. Journal of Huazhong Agricultural University (Social Sciences Edition), 2018(3): 73-80, 156. |

| 崔姹, 王明利, 胡向东. 我国草牧业推进现状、问题及政策建议-基于山西、青海草牧业试点典型区域的调研. 华中农业大学学报(社会科学版), 2018(3): 73-80, 156. | |

| 3 | Bai Y F, Zhao Y J, Wang Y, et al. Assessment of ecosystem services and ecological regionalization of grasslands support establishment of ecological security barriers in northern China. Bulletin of Chinese Academy of Sciences, 2020, 35(6): 675-689. |

| 白永飞, 赵玉金, 王扬, 等. 中国北方草地生态系统服务评估和功能区划助力生态安全屏障建设. 中国科学院院刊, 2020, 35(6): 675-689. | |

| 4 | Fan J D. Fiscal support for the construction of ecological civilization: The 100 year search, experience and prospect of the Communist Party of China. Public Finance Research, 2022(3): 16-25. |

| 樊继达. 财政支持生态文明建设: 中国共产党的百年求索、经验及前瞻. 财政研究, 2022(3): 16-25. | |

| 5 | Han F Q, Li D. The performance analysis of State Grassland Ecological Rewards policy from government action perspective. Journal of Central University of Finance & Economics, 2021(1): 12-20. |

| 韩凤芹, 李丹. 基于政府行为视角的中央财政草原生态保护补助奖励政策效果研究. 中央财经大学学报, 2021(1): 12-20. | |

| 6 | Li D, Wei S. Research on the high-quality development of agricultural insurance-From the perspective of financial subsidies, market competition and product management. Theoretical Investigation, 2021, 218(1): 105-111. |

| 李丹, 魏帅. 农业保险高质量发展探究-基于财政补贴、市场竞争、产品管理视角. 理论探讨, 2021, 218(1): 105-111. | |

| 7 | Pan Q M, Sun J M, Yang Y H, et al. Issues and solutions on grassland restoration and conservation in China. Bulletin of Chinese Academy of Sciences, 2021, 36(6): 666-674. |

| 潘庆民, 孙佳美, 杨元合, 等. 我国草原恢复与保护的问题与对策. 中国科学院院刊, 2021, 36(6): 666-674. | |

| 8 | Zhang J, Wang J H, Yu J Y, et al. Remarkable progress has been made in the pilot construction of grassland insurance in Inner Mongolia. Inner Mongolia Forestry, 2022, 560(7): 12-15. |

| 张瑾, 王建和, 余隽勇, 等. 内蒙古草原保险试点建设成效显著. 内蒙古林业, 2022, 560(7): 12-15. | |

| 9 | Lin H L, Pu Y F, Wang D N, et al. Index insurances for grasslands: A review and the Chinese scheme design. Acta Prataculturae Sinica, 2021, 30(8): 171-185. |

| 林慧龙, 蒲彦妃, 王丹妮, 等. 草原指数保险: 评述与中国方案设计. 草业学报, 2021, 30(8): 171-185. | |

| 10 | Roumiguie A. Insuring forage through satellites: Testing alternative indices against grassland production estimates for France. International Journal of Remote Sensing, 2016(55): 1912-1939. |

| 11 | Feng W L, Liang R. International experience in grassland insurance development. China Finance, 2021, 957(15): 89-90. |

| 冯文丽, 梁瑞. 草原保险发展的国际经验. 中国金融, 2021, 957(15): 89-90. | |

| 12 | Chai Z H, Zhang S Y. Operational mechanism and enlightenment of grassland insurance in America. China Insurance, 2022, 410(2): 58-61. |

| 柴智慧, 张斯媛. 美国草原保险运行机制及启示. 中国保险, 2022, 410(2): 58-61. | |

| 13 | Guo X Y. Research on the risk zoning, product type selection and rate determination of grassland insurance-the case of Xilingol grassland. Hohhot: Inner Mongolia Agricultural University, 2021. |

| 郭新雅. 草原保险的风险区划、产品类型选择及费率厘定研究-以锡林郭勒草原为例. 呼和浩特: 内蒙古农业大学, 2021. | |

| 14 | Shi J H, Wang L, Tian H J. Discussion on the realization form of grassland insurance-Taking grassland insurance as an example in Alukhorqin Banner, Inner Mongolia. Journal of Agricultural Catastrophology, 2022, 12(2): 182-184. |

| 石俊华, 王林, 田海静. 草原保险实现形式的探讨—以内蒙古阿鲁科尔沁旗草原保险试点为例. 农业灾害研究, 2022, 12(2): 182-184. | |

| 15 | Zhang J, Wang J H, Wang B L, et al. Insurance scheme of natural grassland ecological protection and animal husbandry production. Grassland and Prataculture, 2021, 33(4): 39-44. |

| 张瑾, 王建和, 王宝璐, 等. 天然草原生态保护与畜牧业生产保险方案研究. 草原与草业, 2021, 33(4): 39-44. | |

| 16 | Roumiguié A, Jacguin acguin A, Sigel G, et al. Validation of a forage production index (FPI) derived from MODIS fcover time-series using high-resolution satellite imagery: Methodology, results and opportunities. Remote Sensing, 2015, 7(9): 11525-11550. |

| 17 | Li D, Wang X Y, Ma L. Development and experience of pasture, rangeland and forage insurance in the USA. World Forestry Research, 2022, 35(1): 118-123. |

| 李丹, 王馨瑶, 马丽. 美国牧草保险的发展与经验借鉴. 世界林业研究, 2022, 35(1): 118-123. | |

| 18 | Pan T. Agriculture industrialization finance in developed countries empirical analysis of support. World Agriculture, 2015(10): 73-77. |

| 潘婷. 发达国家农业产业化金融支持的经验分析. 世界农业, 2015(10): 73-77. | |

| 19 | Vroege W, Dalhaus T, Finger R. Index insurances for grasslands-A review for Europe and North-Americal. Agricultural Systems, 2019, 168: 101-111. |

| 20 | Finger R, Calanca P, Briner S. Implications of risk attitude and climate change for optimal grassland management: A case study for Switzerland. Crop & Pasture Science, 2014, 65(6): 576. |

| 21 | Boyd M, Porth B, Porth L, et al. The impact of spatial interpolation techniques on spatial basis risk for weather insurance: An application to forage crops. North American Actuarial Journal, 2019, 23(2): 1-22. |

| 22 | Skees J R, Barnett B J. Enhancing microfinance using index-based risk-transfer products. Agricultural Finance Review, 2006, 66(2): 235. |

| 23 | Wu J J. Crop insurance, acreage decisions, and nonpoint-source pollution. American Journal of Agricultural Economics, 1999, 81(2): 305-320. |

| 24 | Hui J W, Bai Z K, Liu K J, et al. Applicability analysis of normalized difference vegetative index (NDVI) in grassland open-pit coal mine. Chinese Journal of Engineering, 2023, 45(1): 54-63. |

| 惠嘉伟, 白中科, 刘凯杰, 等. 归一化植被指数(NDVI)在草原露天煤矿区的适用性分析. 工程科学学报, 2023, 45(1): 54-63. | |

| 25 | Bucheli J, Dalhaus T, Finger R. The optimal drought index for designing weather index insurance. European Review of Agricultural Economics, 2021, 48(3): 573-597. |

| 26 | Roumiguie A, Sigel G, Poilve H, et al. Insuring forage through satellites: Testing alternative indices against grassland production estimates for France. International Journal of Remote Sensing, 2017, 38(7): 1912-1939. |

| 27 | Li S, Zhao S J, Zhang Q. Wisdom agricultural insurance-Prospects of agricultural insurance informatization development. Jiangsu Agricultural Sciences, 2016, 44(1): 7-12. |

| 李舒, 赵思健, 张峭. 智慧农险-农业保险信息化发展的展望. 江苏农业科学, 2016, 44(1): 7-12. | |

| 28 | Xie M H, Wang Q, Meng J H, et al. Compilation method and application of grassland resources balance sheet. Resources Science, 2022, 44(8): 1679-1695. |

| 颉茂华, 王乾, 孟佳慧, 等. 草原资源资产负债表的编制方法及应用. 资源科学, 2022, 44(8): 1679-1695. | |

| 29 | Zhang Y Y, Meng S W. A spatial-temporal dependence model of crop area yield insurance and it’s application. Journal of Applied Statistics and Management, 2022, 41(5): 786-802. |

| 张译元, 孟生旺. 农作物区域产量保险的时空相依模型及其应用. 数理统计与管理, 2022, 41(5): 786-802. | |

| 30 | Li F N, Qin C S, Zhou X, et al. Design of a snow disaster weather-Index insurance for alpine pastoral areas: A case study in Gannan. Acta Prataculturae Sinica, 2021, 30(6): 199-204. |

| 李芙凝, 秦昌胜, 周雪, 等. 高寒草原牧区雪灾指数保险的设计-以甘南牧区为例. 草业学报, 2021, 30(6): 199-204. | |

| 31 | Yu Y. Research on differentiated policy of agricultural insurance premium subsidy based on guarantee level-Experience of the United States and choice of China. Issues in Agricultural Economy, 2013, 34(10): 29-35, 110. |

| 余洋. 基于保障水平的农业保险保费补贴差异化政策研究-美国的经验与中国的选择. 农业经济问题, 2013, 34(10): 29-35, 110. | |

| 32 | Fu L S, Wang S G, Qin T, et al. The incentive effect of forest insurance premium subsidy policy in China: An analysis from the perspective of heterogeneous forest opeeraters. China Rural Survey, 2022, 164(2): 79-97. |

| 富丽莎, 汪三贵, 秦涛, 等. 森林保险保费补贴政策参保激励效应分析-基于异质性营林主体视角. 中国农村观察, 2022, 164(2): 79-97. | |

| 33 | Sun J, Jiang Y Z. Financing mechanism for social long-term care insurance: A theoretical analysis framework. Journal of Jiangxi University of Finance and Economics, 2018, 115(1): 59-68. |

| 孙洁, 蒋悦竹. 社会长期护理保险筹资机制理论分析框架. 江西财经大学学报, 2018, 115(1): 59-68. | |

| 34 | Sun L, Chen S W. The willingness, behaviors to buy agricultural insurance one tropism study and their consistency. Rural Economy, 2021, 469(11): 70-77. |

| 孙乐, 陈盛伟. 农业保险投保意愿、投保行为及其一致性研究-基于解构计划行为理论视角. 农村经济, 2021, 469(11): 70-77. | |

| 35 | Niu H, Wang H S, Chen S W. Insurance participation density, market competition and cost efficiency of agricultural insurance company. The Theory and Practice of Finance and Economics, 2022, 43(5): 33-41. |

| 牛浩, 王洪生, 陈盛伟. 参保密度、市场竞争与农业保险公司的成本费用. 财经理论与实践, 2022, 43(5): 33-41. | |

| 36 | Li J H, Wang G J. Agricultural insurance premium subsidies, agricultural scale and agricultural production level. Journal of Shanxi University of Finance and Economics, 2022, 44(8): 43-57. |

| 李嘉浩, 王国军. 农险保费补贴、农业规模化和农业生产水平. 山西财经大学学报, 2022, 44(8): 43-57. | |

| 37 | Wang Y, Wang J S, Zhang Q. Drought risk status of grassland in China. Acta Prataculturae Sinica, 2022, 31(8): 1-12. |

| 王莺, 王健顺, 张强. 中国草原干旱灾害风险特征研究. 草业学报, 2022, 31(8): 1-12. | |

| 38 | Zou X Y, Fan L. An analysis on calculation and optimization of premium subsidy rate of agricultural insurance in China—Based on incentive and constraint mechanism. Insurance Studies, 2021(8): 3-17. |

| 邹新阳, 范莉. 我国农业保险保费的最优补贴率研究—基于激励与约束机制. 保险研究, 2021(8): 3-17. | |

| 39 | Liu X F, Fu B J. Drought impacts on crop yield: Progress, challenges and prospect. Acta Geographica Sinica, 2021, 76(11): 2632-2646. |

| 刘宪锋, 傅伯杰. 干旱对作物产量影响研究进展与展望. 地理学报, 2021, 76(11): 2632-2646. | |

| 40 | Zhang Y H, Chen H, Li T, et al. Non-standardized products, informal trading relationships and agricultural insurance innovation: the case of policy-based pelagic squid insurance mechanism. Insurance Studies, 2022, 415(11): 10-21. |

| 张跃华, 陈欢, 李彤, 等. 非标准产品、非正式交易与农业保险创新-政策性鱿鱼保险机制研究. 保险研究, 2022, 415(11): 10-21. | |

| 41 | Sun M M, Pei P, He T. Research on insurance technology, operating efficiency, and transmission mechanism. East China Economic Management, 2022, 36(1): 108-118. |

| 孙明明, 裴平, 何涛. 保险科技、经营效率及传导机制研究. 华东经济管理, 2022, 36(1): 108-118. | |

| 42 | Qin T, Li H, Song R. Comparison of forestry carbon sequestration insurance models, constraints and optimization strategies. Rural Economy, 2022, 473(3): 60-66. |

| 秦涛, 李昊, 宋蕊. 林业碳汇保险模式比较、制约因素和优化策略. 农村经济, 2022, 473(3): 60-66. | |

| 43 | Wang X, Xia Y. Optimization of development model and policy creation of income insurance in agricultural planting industry. Economic Review Journal, 2022, 437(4): 96-105. |

| 王鑫, 夏英. 农业种植收入保险发展模式优化及政策创设. 经济纵横, 2022, 437(4): 96-105. |

| No related articles found! |

| 阅读次数 | ||||||

|

全文 |

|

|||||

|

摘要 |

|

|||||